The Trump administration has been aggressive in placing restrictions on China’s semiconductor industry, which I discussed in a September 2, 2020 Seeking Alpha article entitled “China Equipment Suppliers' Threats For Applied Materials And Peers.”

But in a knee-jerk reaction, China is planning a sweeping set of new government policies to expand its domestic semiconductor industry. Beijing is preparing to provide extensive support for the next-generation of semiconductors in the five years to 2025 in its (14th) Five Year Plan.

As a background, in May 2016, the Chinese government officially released the 13th Five Year Plan includes initiatives to promote the construction of 5G wireless networks, accelerating the adoption of internet and e-commerce platforms, and expanding the use of big data and cloud computing.

Despite 13 previous Five Year Plans, a host of initiatives including “Made in China 2025”, and the fact that government funding goes back to 2000 with the “State Council Document 18” to develop its IC industry, the question remains as to whether China can be competitive.

With these plans to become “semiconductor self-sufficient, this article details an extensive analysis of the semiconductor industry in China, and how it currently compares to global semiconductor manufacturers. Two U.S. companies are highlighted: Micron Technology (MU) and Intel (INTC). Both companies, facing increased competition from other non-Chinese semiconductor manufacturers, could be impacted further if China is able to become semiconductor self-sufficient and erode their market share.

China’s Semiconductor Industry

China has been making strides to decrease its dependence on foreign companies who make semiconductors. According to The Information Network’s report entitled "Mainland China's Semiconductor and Equipment Markets: Analysis and Manufacturing Trends," China imported 445.13 billion integrated circuits in 2019, an increase of 6.6% year-on-year; the amount of imports was $305.55 billion, down 2.1% YoY. The export of integrated circuits was 218.7 billion units, an increase of 0.7% YoY; the export value was $101.58 billion, an increase of 20% year-on-year.

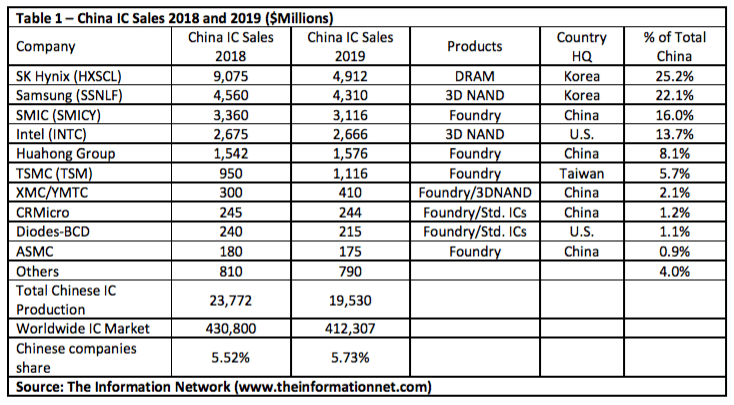

Table 1 shows actual IC production in China in 2018 and 2019. China had to import $101.58 billion worth of chips in 2019. Thus, the $19.5 billion in China-produced chips in 2019 equates to 19% that were “made-in-China”, a bit higher than the 15% of made-in-China semiconductor equipment.

In my above-mentioned September 2, 2020 Seeking Alpha article, I noted that for China’s semiconductor equipment industry in 2019, Chinese suppliers sold just $200 million worth of home-grown equipment compared to imported equipment from foreign suppliers valued at $13.3 billion.

Cumulative shipments of semiconductors into China for 2019 (showing total imports of $305.55 billion as stated above) and 2020 YTD through July. 2020 is on track to reach about $325 billion in imports. That would represent a growth of about 6.4% YoY.

Cumulative shipments of semiconductors into China for 2019 (showing total imports of $305.55 billion as stated above) and 2020 YTD through July. 2020 is on track to reach about $325 billion in imports. That would represent a growth of about 6.4% YoY.

According to WSTS (the industry consortia), total semiconductor growth in 2020 will be 3.3% in 2020, up from a -12.0% growth in 2019. In other words, semiconductor imports into China will be 2X that of growth of the overall semiconductor market.

China’s efforts to reduce gaps in its supply of key technologies and components have largely failed to take off, and there are several important factors impacting China’s semiconductor industry in the near and mid term.

- U.S. Government restrictions on importing products and equipment that could be used by China’s Huawei, which is on the government’s black list.

- New revelations that the U.S. Government may place China’s SMIC (OTCQX:SMICY) foundry on the blacklist. I discussed in a July 17, 2020 Seeking Alpha article entitled “China: Who Needs TSMC When They Have SMIC?” that SMIC was a viable alternative for smartphone chips for Huawei that TSMC was no longer permitted to make.

- Several companies are moving their assembly operations outside China.

- Several IC fabs are ceasing operations in China.

Analysis of Individual Semiconductor Sectors

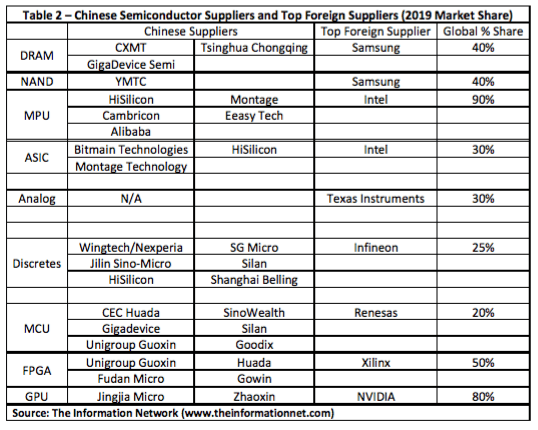

Table 2 organized by decreasing market size of the sector (e.g. DRAM [revenues in 2019] was the largest sector). With few exceptions, Chinese semiconductor suppliers held less than a 1% market share, compared to 20% to 90% market share for the top foreign supplier.

DRAM/NAND

CXMT, GigaDevice Semi, and Tsinghua Chongqing in the DRAM sector and YMTC in the NAND sector have initiated programs to develop a memory industry in China after years of failed attempts to acquire Western companies or, in the case of Fujian, IP (Intellectual Property). In the DRAM and NAND sectors, all Chinese manufactures have <1% market share.

YMTC’s 32-layer NAND in 2018 was three generations behind the main NAND manufacturers. But the jump to 128 layers, effectively bypassing a 96-layer device, makes YMTC's 3D NAND just 2 quarters behind Micron Technology.

CXMT’s DRAMs will be will be at least two generations behind Micron in 2020.

MPU

China does not have any CPU that is not based on Western CPU designs, sometimes they are simply based on ancient CPU designs. While China has the ability to manufacture domestic computer processors, most companies don't use them because they are a generation behind the latest Western processors. All Chinese MPU/CPU manufactures have <1% market share.

Intel has wrestled with problems in transition to a 10 nm process, as it also faced stiffer competition from rivals, led by AMD (AMD). Currently Intel is facing problems with its 7nm process, forcing the company to have its 7nm products manufactured by TSMC (TSM). After two strikes at 14nm and 7nm, Intel says it will make 5nm chips internally, which remains to be seen.

Intel had a 92% share of the MPU market in 2019, with AMD holding a 10% share. But that share has been eroding since 2015 when it held a 97% share, and I expect that share to drop to 89% in 2020. However, market share will not be impacted by Chinese MPU manufacturers, just from AMD.

ASIC

ASIC chips are custom designed and optimized to handle a specific set of functions, so they tend to be significantly superior to general purpose chips in terms of efficiency. ASICs are designed and manufactured for the exclusive use of a single customer.

China's Bitmain, a major customer of TSMC during the cryptocurrency craze of 2018, held a 5% share of the ASIC market in 2019.

Analog

The two largest global suppliers are Texas Instruments (TXN) and Analog Devices (ADI), which make up 50% of the market. There are currently no Chinese analog IC manufacturers. In the Analog sector, all Chinese manufactures have <1% market share.

Discretes

The discrete semiconductor market is highly fragmented, with Infineon holding the largest market share of just 15%, followed by ON Semiconductor with just a 10% share. Nexperia was acquired by Wingtech in late 2019. The company as a 5% share of the Discretes sector.

MCU

The MCU (microcontroller market is dominated by global IDMs including Renasas, NXP Semiconductors (NXPI), Microchip Technology (MCHP), STMicroelectronics (STM), TI, and Infineon (OTCQX:IFNNF).

China has multiple MCU suppliers including Gigadevice, Ingenic, Silan, Datang and CEC Huada. But except for Huada with a 1% share, all have <1% share.

FPGA

Xilinx (XLNX) and Intel account for nearly 90% of the market share, and they have more than 6000 patents. The remaining 10% of the market share is divided between Microsemi (MCHP) and Lattice (LSCC), and these two have more than 3,000 patents. In the FPGA sector, all Chinese manufactures have <1% market share.

GPU

There are only two major companies in the GPU field, one is Nvidia (NVDA), which accounts for about 70% of the market share, and the other is AMD, the second oldest in the world, with a market share of about 30%. In the GPU sector, all Chinese manufactures have <1% market share.

Investor Takeaway

This article attempts to demonstrate that despite billions of US dollars spend bolstering a home-grown semiconductor industry, China is moving further away from its goal of becoming self-sufficient in the industry. Sanctions by the U.S. Government played a part, as it minimized China acquisitions of U.S. chip companies, and restricted access by equipment companies to sell to Chinese companies such as Fujian.

What I’ve also tried to demonstrate that in each of nine major semiconductor sectors, Chinese companies have hardly made a dent in competitive market share. In six of the nine sectors, all Chinese competitors to foreign chip companies held less than a 1% combined market share.

In 2019, China imported $306 billion in chips from foreign companies outside China. Inside China, $102 billion in chips were made. However, just $19.5 billion in chips were made by Chinese companies. The other $80+ billion in chips were made by foreign semiconductor manufacturers located in China, such as Samsung Electronics (OTC:SSNLF), SK Hynix (OTC:HXSCL), and Intel.

Micron Technology, facing increased competition from other non-Chinese semiconductor manufacturers such as Samsung and SK Hynix (Tables 4 and 5), could be impacted further if China is able to become semiconductor self-sufficient and erode their market share. MU is two generations of DRAM ahead of CXMT, but only two quarters ahead of YMTC in 3D NAND.

Intel has had problems with delays in introducing 14nm and now 7nm MPUs into production. In addition, the company is facing erosion in market share from AMD over the past five years. Nevertheless, the company faces minimal competition from Chinese MPU manufacturers.

This free article presents my analysis of this semiconductor sector. A more detailed analysis is available on my Marketplace newsletter site Semiconductor Deep Dive. You can learn more about it here and start a risk free 2 week trial now.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The Link LonkSeptember 10, 2020 at 04:05AM

https://ift.tt/2DKQ8bk

Micron And Intel: Insignificant Threat From China's Chip Companies - Seeking Alpha

https://ift.tt/2YXg8Ic

Intel

No comments:

Post a Comment