MediaTek (TPE:2454) has had a great run on the share market with its stock up by a significant 13% over the last three months. We, however wanted to have a closer look at its key financial indicators as the markets usually pay for long-term fundamentals, and in this case, they don’t look very promising. Particularly, we will be paying attention to MediaTek’s ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company’s success at turning shareholder investments into profits.

Check out our latest analysis for MediaTek

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders’ Equity

So, based on the above formula, the ROE for MediaTek is:

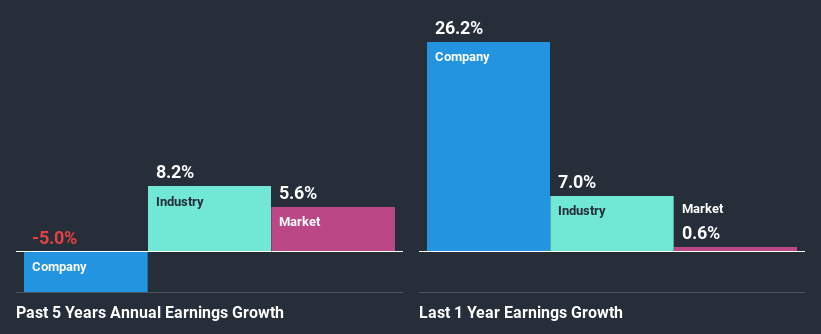

8.2% = NT$26b ÷ NT$324b (Based on the trailing twelve months to June 2020).

The ‘return’ is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each NT$1 of shareholders’ capital it has, the company made NT$0.08 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company’s future earnings. Based on how much of its profits the company chooses to reinvest or “retain”, we are then able to evaluate a company’s future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don’t necessarily bear these characteristics.

MediaTek’s Earnings Growth And 8.2% ROE

At first glance, MediaTek’s ROE doesn’t look very promising. Next, when compared to the average industry ROE of 12%, the company’s ROE leaves us feeling even less enthusiastic. Given the circumstances, the significant decline in net income by 5.0% seen by MediaTek over the last five years is not surprising. However, there could also be other factors causing the earnings to decline. Such as – low earnings retention or poor allocation of capital.

However, when we compared MediaTek’s growth with the industry we found that while the company’s earnings have been shrinking, the industry has seen an earnings growth of 8.2% in the same period. This is quite worrisome.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company’s expected earnings growth (or decline). Doing so will help them establish if the stock’s future looks promising or ominous. Is MediaTek fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is MediaTek Using Its Retained Earnings Effectively?

With a high three-year median payout ratio of 68% (implying that 32% of the profits are retained), most of MediaTek’s profits are being paid to shareholders, which explains the company’s shrinking earnings. With only a little being reinvested into the business, earnings growth would obviously be low or non-existent.

In addition, MediaTek has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 70%. However, MediaTek’s ROE is predicted to rise to 16% despite there being no anticipated change in its payout ratio.

Conclusion

Overall, we would be extremely cautious before making any decision on MediaTek. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. Having said that, looking at current analyst estimates, we found that the company’s earnings growth rate is expected to see a huge improvement. To know more about the company’s future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Promoted

If you’re looking to trade MediaTek, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

The easiest way to discover new investment ideas

Save hours of research when discovering your next investment with Simply Wall St. Looking for companies potentially undervalued based on their future cash flows? Or maybe you’re looking for sustainable dividend payers or high growth potential stocks. Customise your search to easily find new investment opportunities that match your investment goals. And the best thing about it? It’s FREE. Click here to learn more.October 19, 2020 at 10:37AM

https://ift.tt/3kb0wZL

Can MediaTek Inc.’s (TPE:2454) Weak Financials Pull The Plug On The Stock’s Current Momentum On Its Share Price? - Simply Wall St

https://ift.tt/3e1uOdC

Mediatek

No comments:

Post a Comment