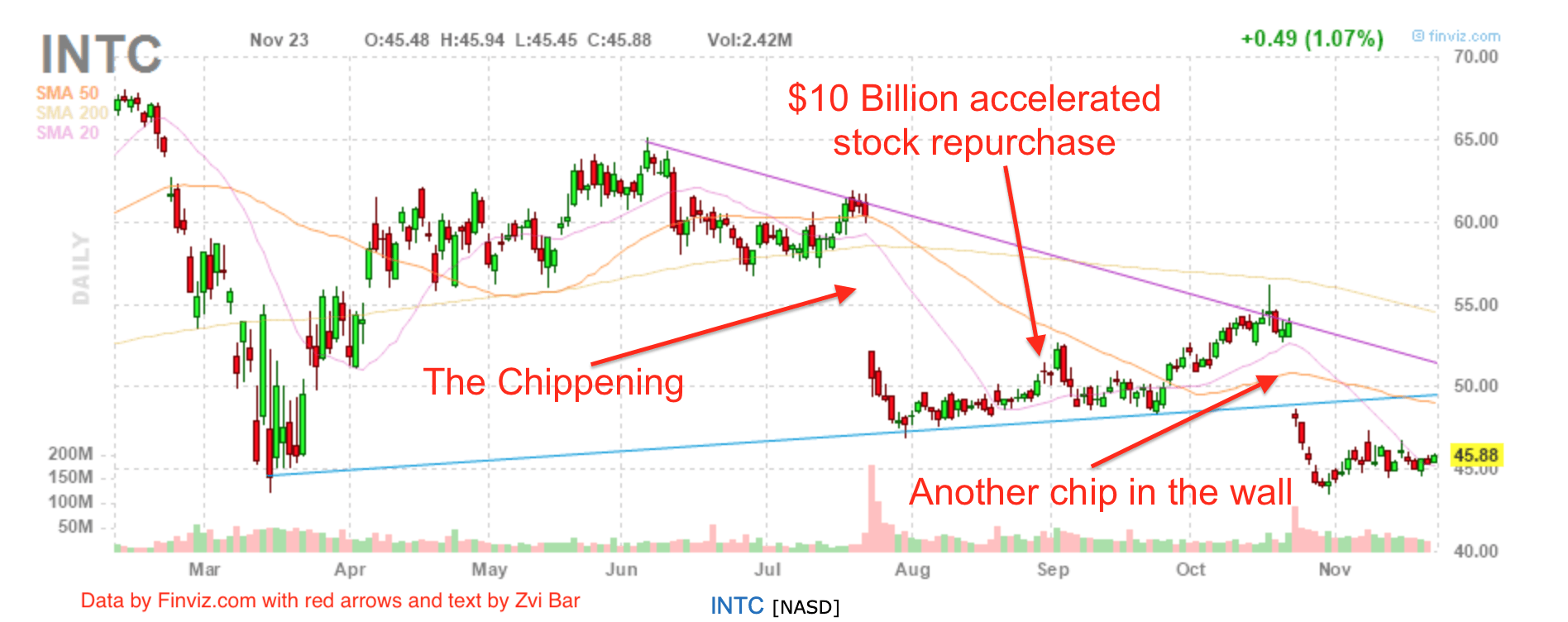

Intel's (INTC) continued failure to promptly address the company's lack of innovation is increasing the probability that its talented competitors will fill that power vacuum. This process is The Chippening, and it is chipping away at Intel's margins, sales, and image. Despite these serious issues, Intel may soon present a strong opportunity, as shares are close to their pandemic low. Prices at or below this range are likely to represent a decent long-term value.

This summer, Intel revealed there would be a delay to its 7nm product due to a defect in the process and, subsequently, terminated its Chief Engineering Officer. I subsequently proposed that Intel must quickly act to acquire new talent and/or technology in order to defend against the apparent power vacuum caused by their lack of technological progress. Since then, both AMD (AMD) and NVIDIA (NVDA) initiated significant M&A deals, while Intel bought its own stock.

NVIDIA locks up ARM

NVIDIA is attempting to acquire ARM Holdings, which is a SoftBank (OTCPK:SFTBY) subsidiary. ARM's chips dominate the touchscreen processing for smartphones and tablets, and really have essentially dominated that market since Apple (AAPL) launched the iPhone. Intel probably assumed it could develop its way into the market, and that regulatory scrutiny would not allow it to acquire ARM.

NVIDIA is not a major competitor within the smartphone and tablet business. It did attempt to compete in the business, but its Tegra chips never got much market share. Acquiring ARM is smart for them, as it should provide NVIDIA with both new technology and differentiated revenue streams.

Apple recently indicated it would change their use of Intel chips in Mac computers to custom made chips that use ARM-based tech. Apple must license ARM's IP in order to make these chips. It is not merely about the cost, as this will not merely improve margins allowing Apple to make an expensive component themselves, but also due to the desire to include a touch screen and improve general efficiency.

This could be the start of a significant transition for chip usage among desktop computers. This may be due to the desire to integrate touch screens, or due to actual efficiencies in running the types of applications that are now being developed for use across multiple platforms. Similarly, this technology appears to be competitive for use in data-centers, where NVIDIA already competes with Intel and others.

AMD links up with Xilinx

Last month, AMD struck a deal to acquire Xilinx (XLNX) in an all-stock transaction valued at $35 billion. The combined company will focus on segments that include data centers, gaming, PCs, communications and automotive, as well as aerospace and other industrial applications.

While Xilinx chips do not have as revolutionary of an application as ARM's technology, their use is incredibly broad and specialized. Xilinx products include platforms for data storage, 5G network radio applications, and other growing industries.

With the addition of Xilinx, AMD will have far more depth to offer large manufacturers. Most major device makes require numerous types of chips, so offering a larger catalog could help AMD win incremental business in some supplemental business lines. This addition makes AMD far more comparable to Intel in terms of offering a diverse catalog of chips, with PC processors at the core. That could also mean that AMD will end up taking more business from Intel in the future.

Intel blows a wad of cash on a buyback

Shortly after speculation NVIDIA's interest in ARM hit the market, Intel announced that it was accelerating its share repurchase plan by buying $10 billion of stock. This was not an additional buyback, but rather part of Intel's previously announced $20 billion share repurchase program, which was initially announced last October and subsequently suspended in March on account of COVID-19 uncertainty or perhaps engineering defects.

With the completion of the accelerated share repurchasing, Intel will have repurchased $17.6B of the $20B it authorized. Intel is likely to provide another repurchase update within the next few quarters, since this plan should deplete enough to require supplementation. Moreover, it appears Intel does not have many other good ideas for what to do with their cash.

Long-term repurchase plans that have a steady flow to them tend to be the most effective ones. This plan attempted to take advantage of a near-term price decline. The acceleration removes the cushion that comes with having a larger pile of cash and a slower flow of repurchases. In any case, it already is apparent that Intel should not have accelerated its repurchasing in August, as INTC shares were then trading at about $50 per share, and are now hovering just above $45.

Moore's law is the observation that the number of transistors within a dense integrated circuit doubles about every two years. The observation is named after Gordon Moore, who was the co-founder of both Fairchild Semiconductor and Intel. This predicted trend requires constant improvement and often radical engineering breakthroughs, including new concepts to chip architecture.

For Intel, maintaining this trend compelled it to develop a Technology, Systems Architecture and Client Group that the company now finds so convoluted and unproductive that they are dividing into five teams. But the real problem here is that with Intel's announcement of falling behind, it appears to have lost much of the allure that it held for several decades. Intel no longer appears as the most formidable competitor in the sector, but rather one needing to catch up to the market.

Competition is tough

Intel's CEO was a fine CFO, but he is unlikely to be very helpful here. Bob Swan was only appointed CFO in 2016, before which he did not work at Intel. The prior CEO resigned in 2018, at which point Bob Swan was made the interim CEO. The company removed the interim in 2019, after what appeared to be a fruitless search for a candidate with semiconductor competence.

The search indicated Intel was aware in needed engineering competence at the help, rather than Swan's financial competence, but they apparently gave up. Bob Swan was a fine CFO and could have been a great CEO if Intel had met its tech development schedule, but he cannot deal with a defect in the company's chips. Meanwhile, the competitors that are moving into the power vacuum have leadership that would be better suited for dealing with Intel's problem.

Nvidia was founded by Jensen Huang, who is its CEO. Prior to founding Nvidia, Huang worked at LSI Logic and AMD, and he has a Master of Science in electrical engineering from Stanford University. Dr. Lisa Su is the CEO of AMD. Dr. Su has a doctorate degree in electrical engineering from the Massachusetts Institute of Technology ("MIT"), has published more than 40 technical articles, was named a Fellow of the Institute of Electronics and Electrical Engineers, and was elected to the National Academy of Engineering.

(Dr. Lisa Su; Source: AMD)

Historically, there was a significant overhang against many semiconductor manufacturers in that there existed the looming threat that Intel could focus on your business and customers. The concern would be that these competitors might lose revenue or suffer reduced margins in an effort to maintain what they had. What is now more probable is that Intel's sales may be vulnerable. At the same time, Intel's competitors appear highly competent and aggressive.

Intel's next move

Fixing the 7nm issue depends upon exactly how bad the defect mode is in the company's process, which is unclear. Until Intel finds itself a suitable solution, it appears to be under the looming danger of being left behind in an incredibly competitive and complicated race.

Intel's next move will probably be more repurchasing. At current levels, Intel's management appears very likely to continue to use excess cash flow to impress upon existing shareholders that they care.

Intel is now dangerously close to the near-term bottom it achieved in March, when the market was in a state of total crisis. It now appears reasonably likely that Intel could retest the low it achieved in March, which was $43.63. I do not think Intel wants that to happen, so I expect the company to launch a new plan in order to fortify this support. Moreover, I believe that if it weren't for Intel's existing accelerated repurchases, Intel would likely be in the low $40s.

I also believe that this is likely to have a very negative effect upon Intel's profit margins in the coming quarters. Analyst estimates will have to be revised to consider the ramifications of declining market share and reduced pricing power upon its profit margins.

Conclusion

Intel remains in a sticky situation. It is facing greater competition than ever before, and simultaneously appears less able to keep up than it used to. While Intel may retest its multi-year bottom, such a move would likely take the company to scrap value. Intel remains likely to underperform peer semiconductors in the near term, but the next dip is likely to present a strong acquisition price.

Disclosure: I am/we are long AAPL, XLNX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The Link LonkNovember 25, 2020 at 10:34PM

https://ift.tt/3lb5Vjk

Intel Deepens In Value - Seeking Alpha

https://ift.tt/2YXg8Ic

Intel

No comments:

Post a Comment