Despite its woes, Intel Corp. remains the largest provider of core processors for “x86” PCs and servers. Its smaller rival for decades has been Advanced Micro Devices Inc. , which has made big strides in the past few years under CEO Lisa Su.

PC manufacturers and users have their preferences. For investors, Advanced Micro Devices AMD, +0.62% has been the clear winner. But Intel INTC, +0.09% has a tremendous R&D budget, has been an excellent cash-flow grower and has enjoyed decades of dominance in its main area of business.

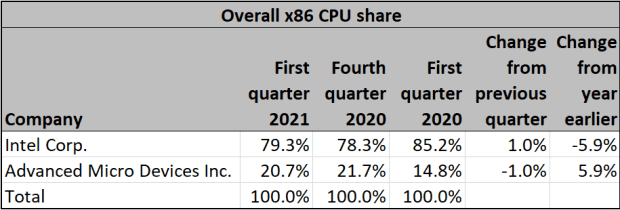

Where Intel and AMD fit in

“Intel is the main supplier of x86 processors and the dominant supplier of x86 server CPUs for data center applications,” according to Dean McCarron, president of Mercury Research, a provider of PC industry data. Most PCs using x86 processors run Microsoft Corp.’s MSFT, -0.09% Windows operating system.

Mercury Research provides market-share data based on unit shipments. Here is its worldwide breakdown for overall x86 CPU market share for the first quarter, with comparisons to the previous and year-earlier quarters:

Intel remains the leader, but you can see that for the first quarter, AMD’s market share increased tremendously from a year earlier. Then again, AMD’s first-quarter share was down a bit from the previous quarter.

For graphics processing units (GPUs), AMD competes with Nvidia Corp. NVDA, +0.33%.

“In the conventional graphics market, Nvidia is dominant, but AMD is also respectably large,” McCarron said.

According to Mercury Research, Nvidia’s share in the conventional GPU market was 81%, with a 19% market share for AMD in the fourth quarter (the most recent for which unit sales data is available).

Competition for data-center GPUs is expected to heat up. Again, Nvidia dominates, as AMD’s market share is less than 10%, according to McCarron. But Intel is expected to begin shipping its own data-center GPUs, code-named Ponte Vecchio, in the fourth quarter or early in 2022.

Key metrics

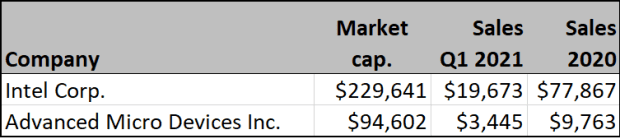

Size and sales

Here are the companies’ sizes by market capitalization and sales, with all figures in millions:

These numbers are fascinating, as they show how much more the stock market values AMD relative to sales. If we divide AMD’s current market cap by first-quarter sales (annualized), we have a price-to-sales ratio of 6.9, against 2.9 for Intel.

The next chart will help explain why.

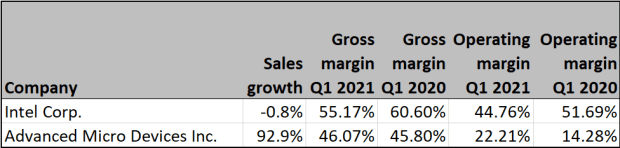

Sales growth and profitability

Here’s a look at both companies’ sales growth for the first quarter from the year-earlier quarter, along with gross margins and operating margins.

Here AMD is the big winner, with first-quarter sales nearly doubling from a year earlier. The overall market is growing and both companies’ sales are increasing, but AMD is giving investors what they want.

A company’s gross margin is its net sales, less the cost of goods or services sold, divided by sales. Net sales exclude returns and discounts. The cost of goods or services sold includes the actual costs for making the items sold or providing the services sold. It doesn’t reflect other overhead expenses. It is a useful measurement of pricing power, and a combination of high sales growth and improved gross margin is a good sign.

Intel’s first-quarter gross margin narrowed, while AMD’s widened.

A company’s operating margin is its earnings before interest, taxes and depreciation divided by net sales. It can be considered “return on sales.”

When comparing the first quarter of 2021 with the year-earlier quarter, you can see a significant narrowing of Intel’s operating margin and improvement for AMD’s operating margin.

One advantage of Intel under CEO Pat Gelsinger, who took up his new position in February, is that Intel can spend so much more on research and development. During the first quarter, Intel spent $3.62 billion on R&D, while AMD spent $610 million.

You can read more about Gelsinger’s strategy and challenges here.

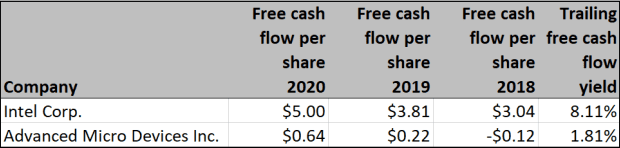

Free cash flow

A company’s free cash flow (FCF) is its remaining cash flow after planned capital expenditures. A company’s free cash flow yield can be calculated by dividing the past 12 months’ free cash flow per share by the current share price.

This chart shows both companies have grown free cash flow over the past three full years, and that Intel has a much higher FCF yield than AMD:

Intel’s FCF yield of 8.11% shows the company has plenty of “headroom” above its current dividend yield, which is 2.44%. (AMD doesn’t pay a dividend.) So Intel is better-positioned than AMD to deploy more cash through expansion, share buybacks or dividend increases.

Intel made both the three- and five-year lists of free-cash-flow compounders, which you can see here.

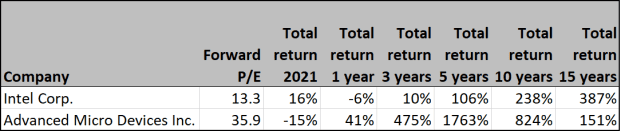

Stock valuation and performance

Here are forward price-to-earnings ratios based on consensus earnings estimates for the next 12 months among analysts polled by FactSet, along with total return figures:

Intel has shined this year, as AMD has pulled back. Intel is also far cheaper when you look at forward price-to-earnings ratios. Those are based on current share prices and consensus earnings estimates for the next 12 months among analysts polled by FactSet. In comparison, forward P/Es are 21.5 for the S&P 500 Index SPX, +0.19%, 27 for the Invesco QQQ Trust QQQ, +0.35% (which tracks the Nasdaq-100 Index) and 20.3 for the iShares PHLX Semiconductor ETF SOXX, +0.27%.

If you review longer periods, AMD has been the clear outperformer, until you look at the 15-year figures.

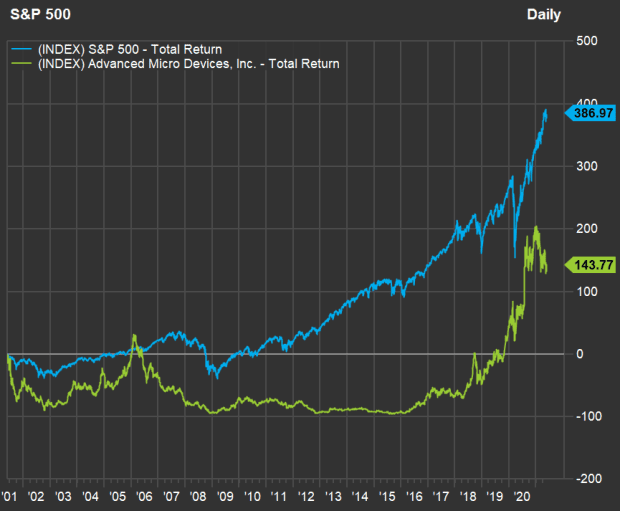

These companies have been competing for the PC CPU market for decades. Here’s a 20-year total-return chart:

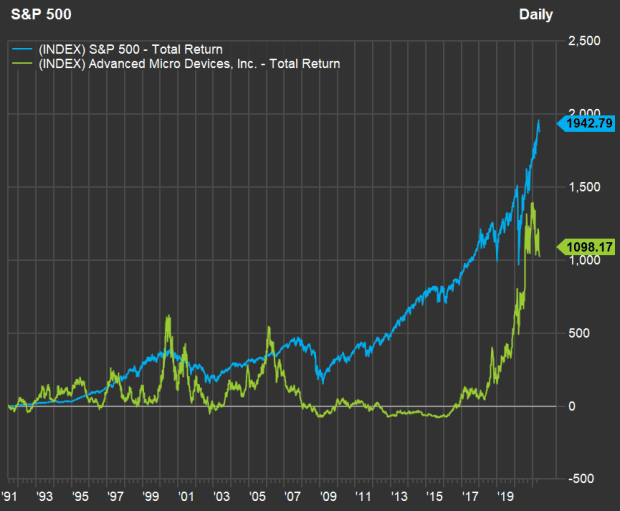

And 30 years:

You can see from the 20- and 30-year charts that these rivals and swung back and forth in the eyes of investors repeatedly.

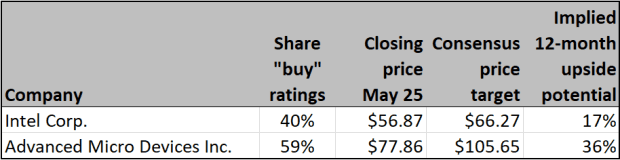

Wall Street’s opinion

AMD is the favorite among analysts at brokerage firms, who expect great things for the stock over the next 12 months:

So there you have a clear contrast — AMD is the up-and-comer, and it has been that way for decades. Intel’s stock is cheaply priced to expected earnings, the company has a new CEO with a new strategy and is trying to move into new areas. Competition for Intel and AMD with Nvidia in the data-center space will be hot — it is a story that will take years to unfold.

Intel has been a tremendous free-cash-flow grower over the long term, as you can see here. AMD is growing very quickly.

So maybe each stock is for a different type of investor. Or maybe investors should consider holding both.

May 26, 2021 at 07:41PM

https://ift.tt/3fnNVmn

Intel vs. AMD — should you buy either stock now? - MarketWatch

https://ift.tt/2YXg8Ic

Intel

No comments:

Post a Comment